Our Blogs

The Environment Industry in India

Concerns about the sustainability of human existence on our earth – keeping in mind the current scenario of enormous population, irresponsible resource harvest, high consumerism, and heavy pollution – have become global. With a hole in the ozone blanket, altering temperature and precipitation patterns, rising sea levels, higher frequency of environmental disasters and many biological species dying out on us, the alarm bells have rung internationally, giving the wake-up call to each and every nation of the world. Governments have been implored to take note of their carbon and water footprints, adopt green policies and low carbon economies, encourage green technologies and practices, and create green collar jobs. There is a good deal of awareness among governments and general public alike regarding the waste generated, the health impacts of pollution and over-all environmental protection.

This indicates that the term ‘Environment’ is no longer restricted to students’ text books or interesting topics of research or altruism-related projects. Environment has now truly emerged as an industry with a wide variety of activities involved, a large global market and high growth potential as a business.

The term ‘Environment Industry’ had been coined as early as 1988 by Environment Business International (EBI) Inc. EBI report 2020 (1988) defines it as “Revenue generation activities associated with environmental protection, assessment, compliance with environmental regulations, pollution control, waste management, remediation of contaminated property and the provision and delivery of environmental resources.” The EU defines it as “producing goods and services used for measuring, preventing, limiting or correcting environment damage to water, air and soil as well as problems related to waste, noise and ecosystems.”

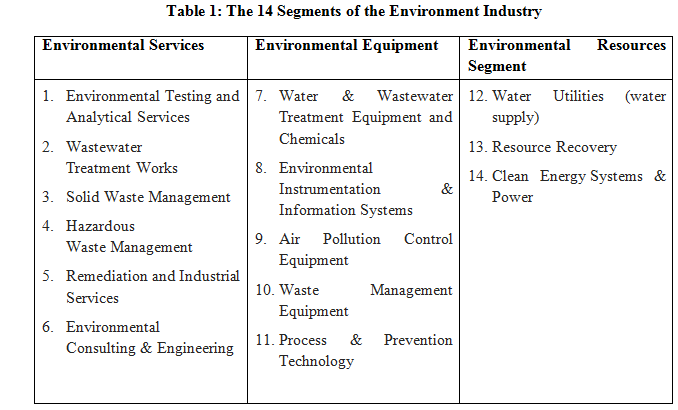

The EBI further classifies the environment industry into 14 segments, which has been provided in Table 1:

Fig. 1: Environment Industry classification

The EBI definition of the environment industry, along with its detailed classification of the 14 segments, was adopted by the US Department of Commerce's Statistical Abstract among other government bodies, chiefly because the North American Industry Classification (NAIC) codes do not cover the environmental goods and services adequately (US ).

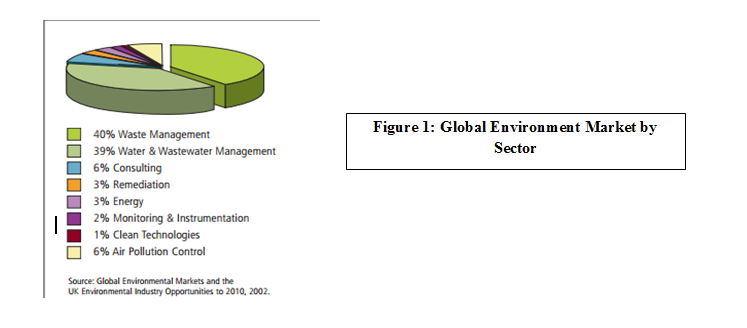

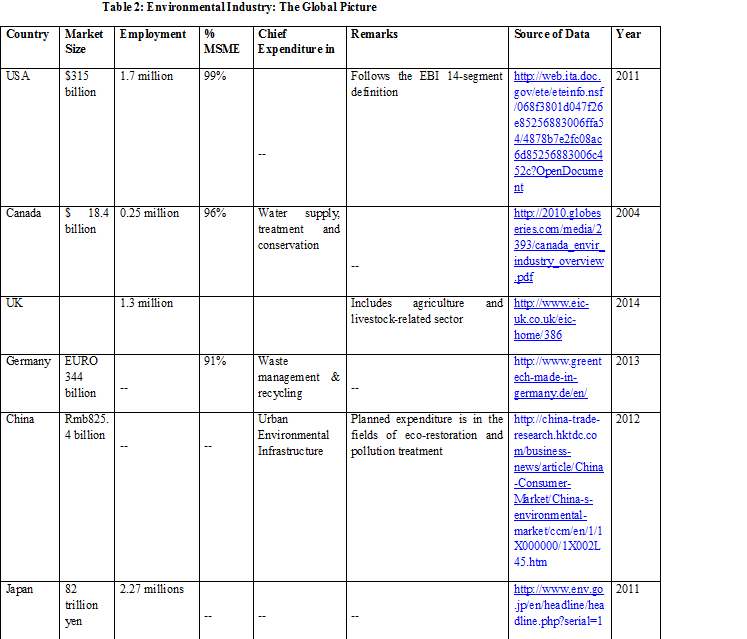

The environment industry is a rather fast-growing sector. Prince Hassan of Jordan, President of the Club of Rome, put this development in a nutshell when he said that “The markets of the future are green.” As per the European Commission, the market for environmental technology grew at an annual rate of 7% from 1999 to 2004. It was valued at $ 803 billion in the year 2010 (EBI Report, 2011). Of this, the USA contributed $315 billion, which is ~ 40% of the total. The USA has about 117,000 enterprises and 1.7 million workers in the environment industry (US census bureau, 2012). Interestingly, ~99% of these are Medium or Small-scale Enterprises (MSMEs); however, these MSMEs together contribute only 20% of the share in income – large enterprises make up 49% and the rest is from local government bodies and public sector entities.

The UK Environment Industry largely includes land or animal-related practices including agriculture and livestock (Lantra 2014). Remarkably, this is in addition to the 14 segments outlined by the EBI. Probably this is why the UK Environment Industry employs about 1.3 million people and 2,30,000 businesses.

The Canadian Environment Industry is also well-defined, with sales worth $ 18.4 billion and 2,51,000 employees (Canadian Govt. Reports, 2004). Interestingly, here too, small firms (fewer than 100 employees) form the majority (96%) of Canada’s environmental companies.

The Chinese Environment Industry includes the equipment manufacturing and engineering of a wide spectrum of technologies and their related services. It includes the provision of equipment and services for environmental pollution control, removal of pollutants, waste treatment, energy conservation, clean production, as well as the collection, secured treatment, recycling and recovery of waste resources. It also covers services related to the protection of resources and the natural ecology. In 2012, the nation’s investment in pollution control and treatment reached Rmb825.4 billion, of which investment in the construction of urban environmental infrastructure accounted for Rmb506.3 billion.

In Japan as well, the environment industry is large, employing 2.27 million people and measuring 82 trillion yen in size (Ministry of Environment, Japan Report 2013). The details discussed above have been compiled in Table 2.

The details discussed above have been compiled in Table 2.

Interestingly, in each and every country discussed here, the government’s environment policy is conducive for development, the environment industry has been showing an increasing trend, ,and, most remarkably, is largely composed of MSMEs.

The Current Scenario

For a set of economic activities to condense into an industry, the following criteria have been discussed by Granovetter and McGuire 1998.

- Development of supporting infrastructure

- Proper definitions of the activities of the industry

- Attainment of legitimacy

Considering this, the environment industry in India is more or less unformulated and rather amoeboid. Activities such as waste recycling, environmental impact assessment, compliances and clearance-related activities, industrial ETP and WWTP set-up and management, environmental monitoring and green technology development (such as solar panels, LED lights, bioengineering-based solutions etc.) are being actively undertaken, but largely by NGOs, government bodies and by a host of unregistered business units, though registered small-scale Pvt. Ltd. entities are also catching up. The Ministry of Environment, Forest and Climate Change, India has a special cell dedicated to the various NGOs active in India, but none for the environmental consultancies or green technology providers!

This is probably because by and large, environmental activities are looked upon as social service to be undertaken by the government and NGOs with an environment-related mandate. A large number of such NGOs are active in India.

Remarkably, such was the picture in the USA as well, as can be gleaned from the quote below:

We have to realize that there is a certain ironic, wry success in that nonprofits all over the country have test-piloted it (recycling) so successfully that big capital has come in and taken over (quoted in Weinberg et al. 2000: 95).

In India, a variety of environment-related legislations have been passed, starting from the Wildlife Protection Act, 1972, with the most recent National Green Tribunal Act 2010. Some of the most relevant ones are Water (Prevention and Control of Pollution) Act, 1974; the Water (Prevention and Control of Pollution) Cess Act, 1977; the Air (Prevention and Control of Pollution) Act, 1981; the Environment (Protection) Act, 1986; Public Liability Insurance Act, 1991; the National Environment Tribunal Act, 1995 and the National Environment Appellate Authority Act, 1997; the Wildlife (Protection) Act, 1972; the Forest (Conservation) Act, 1980. Important from the industrial point of view are the Environment (Protection) Act, 1986, which sets standards for release of fume and effluents for industries, and the Environmental Impact Assessment (EIA) Notification, 2006, making it mandatory for large projects to get an EIA done and get an environmental clearance from the government. The former set into a motion a spate of environmental engineering groups providing turn-key solutions for treating fumes and effluents, while the latter has helped set-up a number of consultancies for getting EIA done and get environmental clearances. Both these set of activities require environmental monitoring and technologies for managing and treating the solid, liquid and gaseous waste generated by the industries.

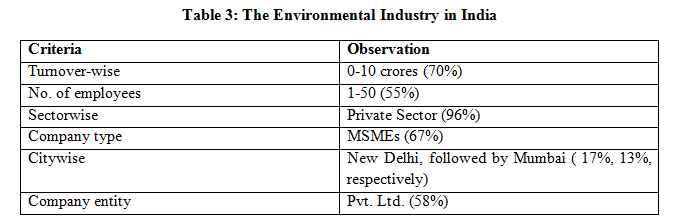

A set of data released by a private website sheds some light on the current scenario of environmental consultancies in India (Table 3):

Source: http://www.fundoodata.com/industry-companies/environment/environment-consultancy/96.html (Total number of surveyed companies – 127)

The Gaps

There remain many gaps in the organization of the environmental industry in India. First and foremost, while the industries have been bound by legalities to control their impact on the environment, it stands to reason that normal citizens release a much larger amount of domestic effluent, municipal solid waste and the potent greenhouse gas carbon dioxide into the atmosphere. No legislation governs them! No private consultancy offers services to them! This domestic effluent and MSW are managed – almost invariably in an inefficient manner – by the local municipalities, aided by the unorganized sector of waste recyclers and NGOs. This is evidenced by the continuously degrading quality of our air, rivers and seawaters and the rising mounds of landfill waste in every city of India.

Another important aspect is that the turn-key solutions of effluent and fume treatment being provided only to the formally registered industries – there exist hoards of unregistered industries in the urban and suburban pockets of India which mindlessly release their hazardous effluents and fumes into the environment, meeting no norms, and getting no EIA.

Also, the engineering-based turn-key solutions being offered to industries are far from perfect – their operating cost is high, often tempting unscrupulous industries to release their waste untreated into the environment. Many of these treatment technologies are imported from abroad and rather expensive. Hence, the requirement of green technologies, which are suitable for the Indian context, are low on cost and energy requirement – and keeping in mind the cradle-to-cradle approach – actually generate a useful, saleable end product – is undeniable. In fact, it is absolutely necessary.

India is an agricultural country and the contribution of agriculture to pollution is notable. Mindless application of unrequired amounts of chemical fertilizers and pesticides to farms has caused a large amount of damage to the top soil – causing salinity levels to increase significantly in many areas. Agricultural run-off – containing unused fertilizers and pesticides – have created havoc in the water bodies they drain into – causing eutrophication and biomagnification of xenobiotics. Agricultural solid waste is largely organic in nature and is usually utilized by the village folk as fuel, housing material, fodder or natural manure.

The Formalization Process

Some sort of formalization has been initiated through the NABET accreditation of individuals and organizations involved in the EIA process. The National Accreditation Board for Education & Training (NABET), a constituent board of the QCI, initially developed a voluntary accreditation scheme with inputs from various stakeholders including experts in the field, regulatory agencies, consultants etc., and launched it in August 2007. Some of the leading consultants in the field obtained accreditation under the scheme. The Ministry of Environment, Forests and Climate Change (MOEF) reviewed the scheme in 2009 and desired that the Scheme be updated incorporating the learning since launching of the Scheme. The Scheme was made mandatory by the MOEF through an Office Memorandum dated December 2, 2009.

The job of EIA is done by qualified and experienced individuals who are called Functional Area Experts and EIA coordinators and have received such certification from the NABET of Quality Council of India (QCI). Some of these accredited professionals are empanelled with one of the many environmental consultancies, while many of them operate independently as freelancers. NABET also provides accreditation to environmental consultancies. The latest list of NABET accredited organizations numbers as less as 171.

The picture presented above is minimalistic – and has not been formally reported in peer-reviewed journals or government papers. It has been largely derived from personal experience and observations. Hence, the scope of formal and statistically sound research in this field is clearly indicated.

THE DHARAVI CASE STUDY

These authors had conducted a focus-group based in Dharavi, the infamous slums of Mumbai. Dharavi is actually an economically sound, well-oiled machinery of a large number of unregistered, informal businesses in the MSME sector. Of this, a sizeable chunk is of waste recyclers. The waste recycling industry of Dharavi presents a clear picture of how unclear we are regarding the informal sector and how important a role this sector plays in the unshaped environmental industry of India. The study was conducted in the months of August-October, 2014.

Study Area – Geographical, Socio-Economic and Historical Details

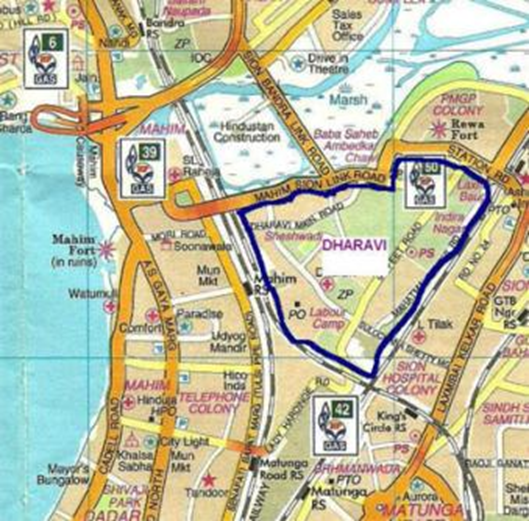

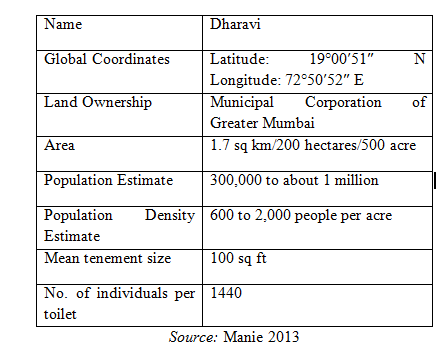

The slums of Dharavi in Mumbai have earned the dubious distinction of being one of the largest in the world (Sharma 2000). Geographically, Dharavi spreads across 175 ha (1.7 sq km) government-owned land right in the heart of the Mumbai city with Mahim in the west and Sion in the east (Figure 1). It is a densely populated region with estimates ranging from 600-2000 people/acre. Various significant details of Dharavi have been summarized in Table 4.

The Oxford dictionary describes the word ‘slum’ as “a squalid and overcrowded urban street or district inhabited by very poor people.” Considering this, Dharavi is indeed a slum with squalid, sunless 100 sq ft corrugated tin-roof settlements for eight-member families, open drains, the lack of toilets and extremely difficult and inhuman living conditions that one observes here not being hidden from anyone.

Dharavi has two sections – residential and commercial. The commercial section has about 10-15 thousand single-room industrial units involved in solid waste recycling, machine spare part making, leather-tanning, shoe-making, textile-dyeing, stitching, embroidery, block-printing, pottery-making and baking. The annual turnover from these industries is as much as $650 million dollars (Bansal and Gandhi, 2012). Many products formulated here are sold in the native markets and also exported worldwide.

Dharavi may be described as an inter-city township (Patel and Arputham 2008), which sustains itself with little or no outside support. One of the most unusual industries to have found its way inside Dharavi is the tourism industry, with slum or reality tours gaining immense popularity post ‘Slumdog Millionaire’ (Dyson 2012, Bansal and Gandhi 2012).

Survey Details

The methodology of Focus Group was followed. A focus group is an in-depth, open-ended group discussion of 1-2 hours' duration that explores a specific set of issues on a predefined topic. Such groups consist of 6-8 participants and are arranged under the guidance of a facilitator. The survey was conducted during the month of August 2014. Here, groups of plastic recycling industry owners and workers were targeted. Group size ranged from 5-10.

RESULTS AND DISCUSSION

The study involved a total of 10 groups of average size 8. Dharavi has about 1200 units of waste recycling, of which 780 were of plastic recycling. The survey results provide information on direct impact of recycling industry. The direct impact can be calculated by the initial spending or job generated by the firm engaged in recycling activities. Apart from direct impacts, recycling industry has many indirect effects in economy and society. Overall economic impact of the recycling industry has “ripple effects.”

In a recycling facility, the plant hires workers and pays a payroll. The operations of the plant are the direct expenditures. In the process of its operations the firm may purchase goods and services from other companies. These purchases are termed the “indirect impacts.” For example, a recyclable materials processor purchases machinery from machinery manufacturers who in turn purchase raw materials, parts, and services from other industries.

Procedural Details

Waste recycling units in Dharavi have an informal supply and delivery chain with local rag-pickers at one end and large industrial units at the other. Most of the work is done manually, with women being employed in some areas. According to the Mumbai Metropolitan Regional Development Authority (MMRDA), 11,209 tonnes of waste is generated /day and the vast majority comes to Dharavi. On average, each waste-picker sorts through 8.5 tonnes of rubbish each day. Almost 80% waste in Mumbai is recycled, as compared to 23% in the UK.

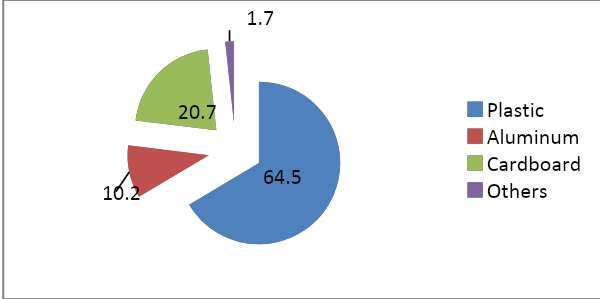

~1200 waste recycling industries exist in Dharavi. Of these, 780 units were those of plastic recycling (Figure 2), others being that of aluminium, cardboard box and paper recycling and a few units of glass crushing. Raw material for these units is obtained not only from the local rag-pickers but also from all over India. ~ 70% units were unregistered.

Plastic recycling process is partially carried out in Dharavi. It employs the sourcing of plastic waste locally and even from other states of India and its sorting. After sorting, waste is cleaned and dried on roof-tops. Post this, waste is crushed in an electricity-run crushing machine and dyed. Same-coloured plastic is converted into pellets mechanically, which are sold for further processing.

The chief investment made by the entrepreneurs is in the purchase of the Dharavi building and the plastic crushing machine. The former is in the range of INR 3,00,000-5,00,000 while the latter costs about INR 75,000-1,00,000. In addition, the entrepreneur pays a monthly rent to the Municipal Corporation of Greater Mumbai (MCGM) of INR 1200/-. The process costs of recycling plastic comes to INR 20/kg.

Socio-economic Details

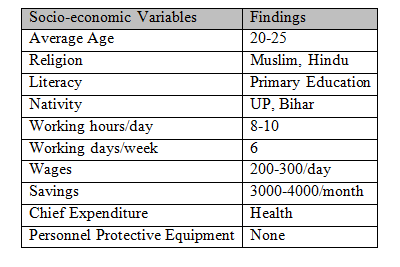

Most of the business owners of recycling units were Muslims. Several owners confirmed they were residents of Dharavi and the business was family-owned. A few others were from outside, who had shifted here due to cheaper availability of resources. However, many owners had shifted their residents outside Dharavi where living conditions were better, while retaining their industrial units.

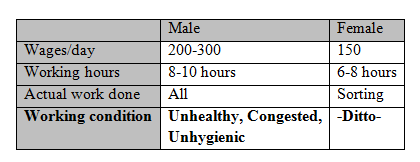

Wage Structure

Male workers were paid INR 200-300/day. Normally, they worked for about 10-12 hours/day for six days a week. Average age was ~ 25.6 years. Workers were mostly migrants from Uttar Pradesh and Bihar. They were illiterate to barely literate and extremely poor. Almost all workers had migrated singly, leaving their families in their native places. After working 8-9 months and collecting some money they returned home, but resumed after 3-4 months. Their health condition was not satisfactory.

Neither workers nor owners had any formal social security. Workers – both men and especially women were underpaid. While water was free-of-cost for most of the units, some owners reported a water meter and a water bill of INR 350-400/month.

Chief expenditure was in health expenses, both by workers and business owners. Reason of health loss or frequent illness was very clear. The work environment was unhygienic, with no ventilation and cleanliness. No health security measure was provided to the workers who worked without sunlight, fresh air, clean water, toilets and also without personnel protective equipment such as helmets, gloves, boots and masks.

Job-hopping or attrition rate was surprisingly low despite appalling work conditions, because workers were not trained for any other process and suffered from poor literacy and awareness levels.

Women were employed for waste sorting. No child labourers were observed.

Average income of workers in all the waste recycling units ranged between INR 1000-4000/month. It was ~INR 10,000-25,000 for the owners.

Waste being sorted and washed may contain hazardous chemicals, which can harm the workers handling it. Noise pollution during plastic-crushing was significant. Health hazards were also observed because of over-all unhealthy living conditions. Due to very few toilets (only two in the industrial section), workers were forced into open defecation, leading to gastro-intestinal infections. Sun-less conditions of Dharavi workplaces and proximity with Mahim Bay and open nalas made mosquitoes a major problem.

Plastic recycling industries, in general, involve only sorting, washing, crushing, dyeing and pelleting of plastic. Plastic waste may be contaminated with hazardous chemicals, oil and grease and other materials, which will be touched by the workers during handling and dissolve or mingle with water used for washing. Its crushing in a machine creates noise pollution. The spent dyes used in colouring the plastic are not disposed properly in the absence of an effluent treatment plant.

People-Centred: Recycling industry at Dharavi is working with a people-centric approach, insuring long-term benefits for the marginalized groups of Mumbai slum-dwellers.

Long-term vision of conserving resources and environment: This industry has a long-term vision with a clear goal of providing employment and conserving environment.

Comprehensive and Integrated: Recycling industry has adopted comprehensive and integrated approach where economic, social and environment objectives are taken care of. However, considerable efforts are needed to make it more competitive.

Conclusion and Future Scope of Work

Dharavi’s recycling zone can be the way forward to a sustainable future. Dharavi is a teeming centre of small-scale industries, but the challenges faced by workers here are massive. It is imperative that the Indian Government intervenes, gets all the units registered, provides financial and health security to the workers and improves the living and working conditions. The future scope of work in this area is enormous from the socio-economic point of view. More detailed surveys must be carried out to glean all possible information regarding the various businesses thriving in Dharavi. Also, the business model of the waste recycling and other industries housed at Dharavi needs to be scrutinized in detail and compared with other existing models in India and abroad so that their productivity is retained while living and working conditions are improved.

Recommendations

A re-development of Dharavi is on the cards. This must take into account the unique history and spirit of Dharavi. A typical housing society with high rises, concretized gardens, malls and multiplexes is highly unsuitable. It is more important to retain all the activities taking place at Dharavi while making them more airy, sunlit, spacious and with toilets.

CONCLUSIONS AND RECOMMENDATIONS FOR GROWING THE ENVIRONMENT INDUSTRY IN INDIA

- Encouragement to environmental entrepreneurs

- Adopting a conservation-oriented approach towards the environment, instead of preservation-oriented, wherever feasible. This means drafting a sustainable-harvest plan from a given ecosystem

- Registration of the currently unregistered units involved in the various green collar jobs, to bring this largely informal sector within the folds of the formal sector

- Introduction of state-of-the-art technology, especially in the job of solid waste management and waste recycling

- Encouragement to cutting edge research in green technology development

- Provision of health benefits to the labourers involved

- Adjusting for machine-induced unemployment – training the unskilled hands and absorbing them within the new system

- Better implementation of existing legal frameworks

- Developing community-based management of the environment as a segment of the environment industry

- Raising immense environmental awareness among all and sundry

- Promoting environmental ethics – reducing consumerism, enhancing community living, bridging the gap between man and nature

References

Bansal R and Gandhi D (2012) Audio Book “Poor Little Rich Slum”, Westland India, Mumbai

Dyson P. (2012) Slum Tourism: Representing and Interpreting ‘Reality’ in Dharavi, Mumbai.

volume 14, Issue 2, Special Issue: Global Perspectives on Slum Tourism. Tourism Geographies: An International Journal of Tourism Space, Place and Environment

EBI Report 2020: The U.S. Environmental Industry and Global Market (Environmental Business International Inc.), p.12

Environmental Industry—Revenues and Employment by Industry Segment: 2000 to 2010," in Statistical Abstract of the United States: 2012, (U.S. Census Bureau), Table 380, p.12

Granovetter, M. and McGuire, P. (1998). The Making of an Industry: Electricity in the United States. In M. Callon (Ed.), The Laws of The Markets (pp. 147-173). Oxford, U.K.: Blackwell

Sharma, Kalpana (2000) "Rediscovering Dharavi: Story From Asia's Largest Slum" Penguin Books

Sheela Patel and Jockin Arputham, (2007) 19: 501 Environment and Urbanisation

Sheela Patel and Jockin Arputham, (2008) Plans for Dharavi: negotiating a reconciliation between a state-driven market redevelopment and residents' aspirations 20:243 Environment and Urbanisation

Statistics Canada, Environment Accounts and Statistics Division, Environment Industry Survey, (2004).

The Canadian Council for Human Resources in the Environment Industry, Environmental Labour Market (ELM) Report, 2004.

http://www.qcin.org/nabet/EIA/documents/Accredited%20consultants.pdf